A sold exhibition floor says more about an industry than a panel title.

ONS 2026 will be held in Stavanger from 24 to 27 August. The official theme is “Courage,” framed around energy insecurity, geopolitical tension, climate pressure, innovation and difficult decisions shaping the next phase of the energy market.

Fine. That is the language on the front door.

The harder signal is inside the building. The full Strategic Conference Pass costs NOK 20,900, plus VAT. The standard ONS Ticket costs NOK 600, plus VAT. ONS+ downtown Stavanger is free and open to the public, with debates and networking in the city. That tells you something about how the industry is forced to operate now: executives upstairs, suppliers on the floor, public legitimacy outside in the streets. Strategy, sales and explanation all running at the same time.

But forget the speeches for a moment.

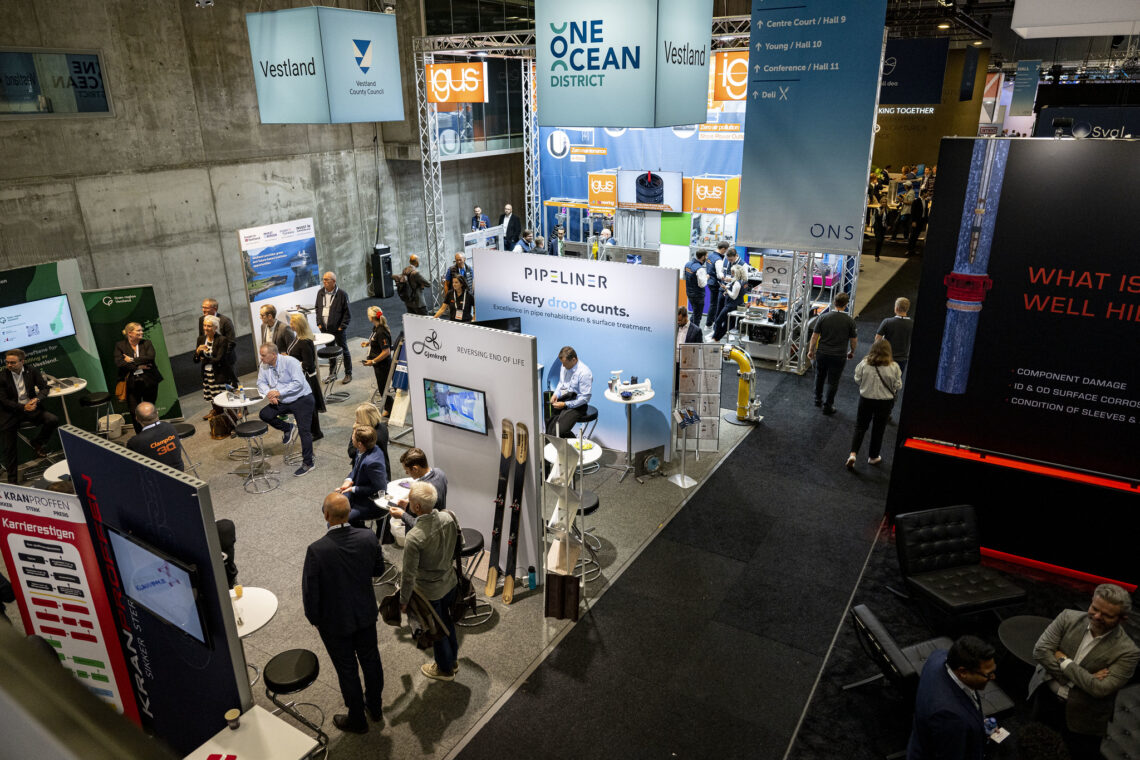

ONS lists scale figures few energy events can match: 72,676 visitors, more than 1,100 exhibitors, more than 1,150 speakers and participants from 102 countries. The 2026 exhibition space is already more than 95 percent sold out.

That is not event decoration. It is market evidence.

Companies do not book exhibition space, send teams to Stavanger and spend money on visibility because an industry is drifting quietly toward irrelevance. They do it because contracts are still being pursued, technology still has to be sold, projects still need suppliers, and the energy transition itself requires a deep industrial base. That is the part of the transition debate that often gets polished out. Someone still has to build, weld, install, maintain, inspect, repair and replace the physical system that keeps Europe running. The language may be about transformation. The work is still steel, pressure, cables, vessels, substations, pipes, safety systems and people who know what weather does to a plan.

This is where Stavanger matters.

Stavanger remains one of Europe’s key energy clusters as supply security, offshore competence and transition investment converge. Photo source: ONS / Carina Johansen

The city is not important because it hosts an energy conference. It hosts an energy conference because the competence is already there. Stavanger represents a mature energy cluster with engineering depth, supplier networks and offshore experience built over decades. That competence was created by oil and gas. Much of it will also be needed for whatever comes next.

The transition does not remove heavy industry from the equation. It drags it deeper in.

Offshore wind still needs vessels, ports, cables, maintenance crews and people who understand harsh conditions at sea. Carbon capture needs pipes, compressors, storage knowledge, monitoring and industrial discipline. Electrification needs grids, substations, permits, equipment and years of work that cannot be summoned into existence by a press release. Hydrogen, batteries, digital systems, lower-emission production — all of it sounds smoother in a strategy document than it looks on the ground. There is mud in this. There are delays. There are ships that cost money whether the political mood is elegant or not.

This is where the neat political logic starts to fall apart.

Europe has spent years discussing energy as if targets could substitute for supply. They cannot. A climate target does not power a factory. A subsidy does not by itself build a grid. A political deadline does not replace reliable gas when electricity demand rises, weather turns cold or geopolitical risk becomes immediate. The public debate can pretend those tensions are temporary. Industrial users cannot.

Data leading into the 2026 cycle shows why Norway’s position remains central.

In 2024, Norway exported a gas volume equivalent to more than 30 percent of total gas consumption in the EU and the United Kingdom. For a small country, that is a large strategic role. For European buyers, Norwegian gas is not only a commodity. It is supply from a stable producer, delivered through existing infrastructure, at a time when Europe has had to reduce dependence on Russia and live with the cost of its own energy choices.

That is not theory. It is volume.

Which brings us back to the real bottleneck: not ambition, but delivery. Norway is now Europe’s primary natural gas supplier. Equinor and its partners are investing just over NOK 4 billion in a new subsea development to increase gas production from the Troll field in the North Sea. The project has a brutally simple commercial logic: more gas to Europe, using existing infrastructure, standardisation and reuse to reduce costs and speed up delivery.

That is the harder version of energy realism: money spent on existing fields because Europe still needs the gas.

It is not the clean break often implied in political language. It is the careful extension of a system Europe still depends on while companies and governments try to build something lower-emission beside it. The Troll investment points to the logic now shaping much of the sector: keep reliable production going, control costs, use existing infrastructure better and maintain supply while new systems mature. No neat slogan sits comfortably on top of that. Good. It should not.

ONS 2026 will naturally speak about transformation, new technology and sustainability. Some of that will matter. Some of it will be ceremonial. The commercial activity around the event points to something rougher and more useful. The industry is not gathering in Stavanger merely to discuss the future. It is gathering because the present remains expensive, technical and unresolved.

Energy companies face a narrow corridor. They are expected to reduce emissions, secure supply, satisfy governments, defend capital discipline and still deliver returns. Suppliers face the same pressure in practical form. They must serve existing oil and gas projects while positioning themselves for newer markets that may take longer to mature than politicians prefer to admit. That is not a branding problem. It is an order-book problem.

Public language can move quickly; infrastructure cannot.

Projects still depend on regulatory certainty, permitting speed, grid capacity, supplier depth and public trust. Industrial users need reliable power and heat now, not only a pathway document for 2035. Investors need stability before they commit long-term capital. Suppliers need contracts, not transition rhetoric dressed up as demand. This is what ONS gathers in one place: the people selling equipment, the executives trying to justify investment, the politicians trying to sound serious, and the industry’s awkward need to be both old and new at the same time.

There is a temptation to make this cleaner than it is.

A country that produces oil and gas can still invest in new technology. A company that develops offshore fields can still reduce emissions. A continent that wants more renewables can still need gas. These are not contradictions in the real economy. They are contradictions mainly in political language, where energy is often discussed as if one system politely exits the room before the next one enters.

It does not work like that.

ONS sits in that tension because the energy sector itself now sits there. It is a conference, an exhibition floor, a deal-making arena and a public ritual. Executives come to position themselves. Suppliers come to sell. Politicians come to signal. Start-ups come to be discovered. Critics come because the industry remains politically sensitive. All of that matters, but it is not the centre of the story.

The centre is work.

Welders, engineers, seafarers and maintenance crews. Steel, ships, safety systems. Competence built over decades, not announced in a panel session. The people who know where the weak points are. The suppliers who know what breaks, what corrodes, what takes six months longer than promised and what happens when a system designed on paper meets salt water, wind and a hard deadline.

That is why the “Courage” theme is more interesting than it first appears. The safe version of courage is to repeat the approved transition language. The more serious version is to admit that Europe’s transition depends on the same industrial competence many policymakers treat as yesterday’s problem.

The bookings suggest the market already understands this.

The sold exhibition space, the ticket structure, the Troll investment and Norway’s gas position all point in the same direction. Europe’s energy future will not be built by pretending the old system has already disappeared. It will be built by companies, workers and investors who can keep the existing system functioning while building the next one.

ONS 2026 will bring the familiar language of transformation. The better story will be found in who comes to Stavanger, what they are selling, what they are financing and what Europe still needs when the speeches are over.

Stavanger is not a relic of Europe’s energy past. It remains one of the places where Europe’s energy future has to be negotiated, financed and built.